$500 a Month for 20 Years: What Compound Interest Realistically Looks Like

Key Takeaway

Investing $500 a month for 20 years at a 7% average annual return gives you roughly $260,000. About half of that is money you never contributed. At 10%, it's closer to $344,000. Compound interest is real, but it's not magic. It rewards patience, not perfection. The earlier you start, the more the math works in your favor. You can model your own numbers with the DecentWealth Investment Calculator, free, no account required.

There's a certain genre of financial content that loves to tell you compound interest is the eighth wonder of the world. Usually attributed to Einstein (who almost certainly never said it). Usually followed by a chart that goes from $0 to $3 million on a timeline that conveniently ends at age 85.

That's not how most people think about their money. Most people think:

I can put away $500 a month. What does that actually turn into? And should I bother?

Let's answer that honestly.

The baseline: $500 a month, 20 years, 7% return

If you invest $500 every month into a diversified portfolio (think total market index funds or a mix of ETFs), the long-term average return of the U.S. stock market gives you a reasonable planning number: roughly 7% annually after inflation.

Here's what that looks like:

- Total contributed out of your pocket: $120,000

- Portfolio value after 20 years: ~$260,464

- Interest earned (money you never touched): ~$140,464

So you put in $120K over two decades, and the market handed you an extra $140K on top. More than you contributed. That's the compounding part doing its job.

It's not a Lamborghini. It's a life-changing amount of financial breathing room that grew quietly in the background while you were doing other things.

What changes if the market does better (or worse)

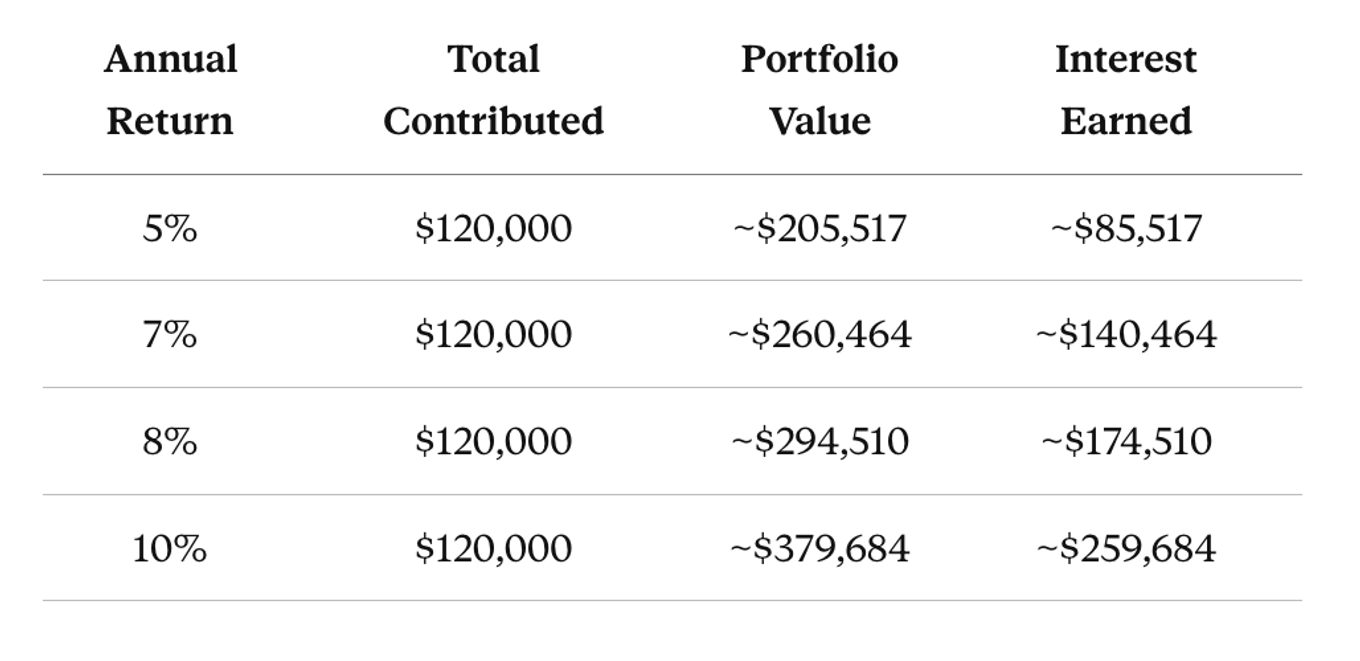

Nobody gets a flat 7% every single year. Some years the market drops 20%. Some years it rips 30%. Over long stretches, though, the average tends to settle. Here's the same $500/month at different return rates:

A few things jump out. The difference between 5% and 10% isn't just "a little more." At 10%, the interest earned is more than double your total contributions. At 5%, it's still meaningful, but the heavy lifting is mostly yours.

This is why return assumptions matter. A lot of compound interest content uses 10% or 12% because it makes the chart look incredible. And yes, the S&P 500 has averaged about 10.2% annually since 1957, before inflation. After inflation, it's closer to 7%.

Planning with 7% is honest. Getting 10% is a bonus. Planning with 12% is a vision board, not a financial plan.

The part nobody talks about: the first five years are boring

Here's the uncomfortable truth about compound interest. For the first several years, it barely does anything. You're basically just watching your own contributions pile up with a modest return on top.

At the 5-year mark with $500/month at 7%, your portfolio is worth about $35,796. You contributed $30,000 of that. The compounding added less than $6,000.

Not exactly life-changing, right?

But this is the part where most people quit. They look at their account after two or three years, see gains that could've been earned from a decent side gig, and wonder if it's even worth it.

It is. Because compound interest is a slow burn that turns into a wildfire. The gains in years 15 through 20 are dramatically larger than the gains in years 1 through 5, even though you're contributing the same $500 every month. By year 20, your money is earning more in a single year than you contribute all year.

That's the inflection point. You just have to survive the boring part to get there.

Starting at 25 vs. starting at 35: the $100K gap

This is where the math gets personal. Let's say two people both invest $500/month at 7%, and both plan to check in at age 55.

Person A starts at 25. They invest for 30 years.

- Total contributed: $180,000

- Portfolio value: ~$609,985

- Interest earned: ~$429,985

Person B starts at 35. They invest for 20 years.

- Total contributed: $120,000

- Portfolio value: ~$260,464

- Interest earned: ~$140,464

Person A contributed only $60,000 more. But their portfolio is worth $349,000 more. That extra decade of compounding added over a third of a million dollars, and most of it came from returns on returns on returns. Not from extra effort.

This isn't meant to make anyone who started later feel bad. Starting at 35 with $500/month still gets you to $260K. That's a real number. But if you're 25 and reading this and thinking "I'll start investing later when I make more money," this is your sign to reconsider. Time is the variable that matters most, and it's the only one you can't buy back.

Track what you're building

There's a reason people abandon their investment plan after a couple of years. It's not laziness. It's that they can't see the progress. Contributions go out, time passes, and the number in their brokerage moves in ways that feel random.

Having a clear view of your total portfolio, including what you contributed versus what the market gave you, changes how you feel about the process. It turns an abstract number into a story. Your story.

DecentWealth is an investment portfolio overview for iPhone that shows your full net worth across stocks, ETFs, crypto, real estate, and more. No account, no email, no data leaving your device. Just your numbers, on your phone.

Download DecentWealth free on the App Store to track your real portfolio privately.

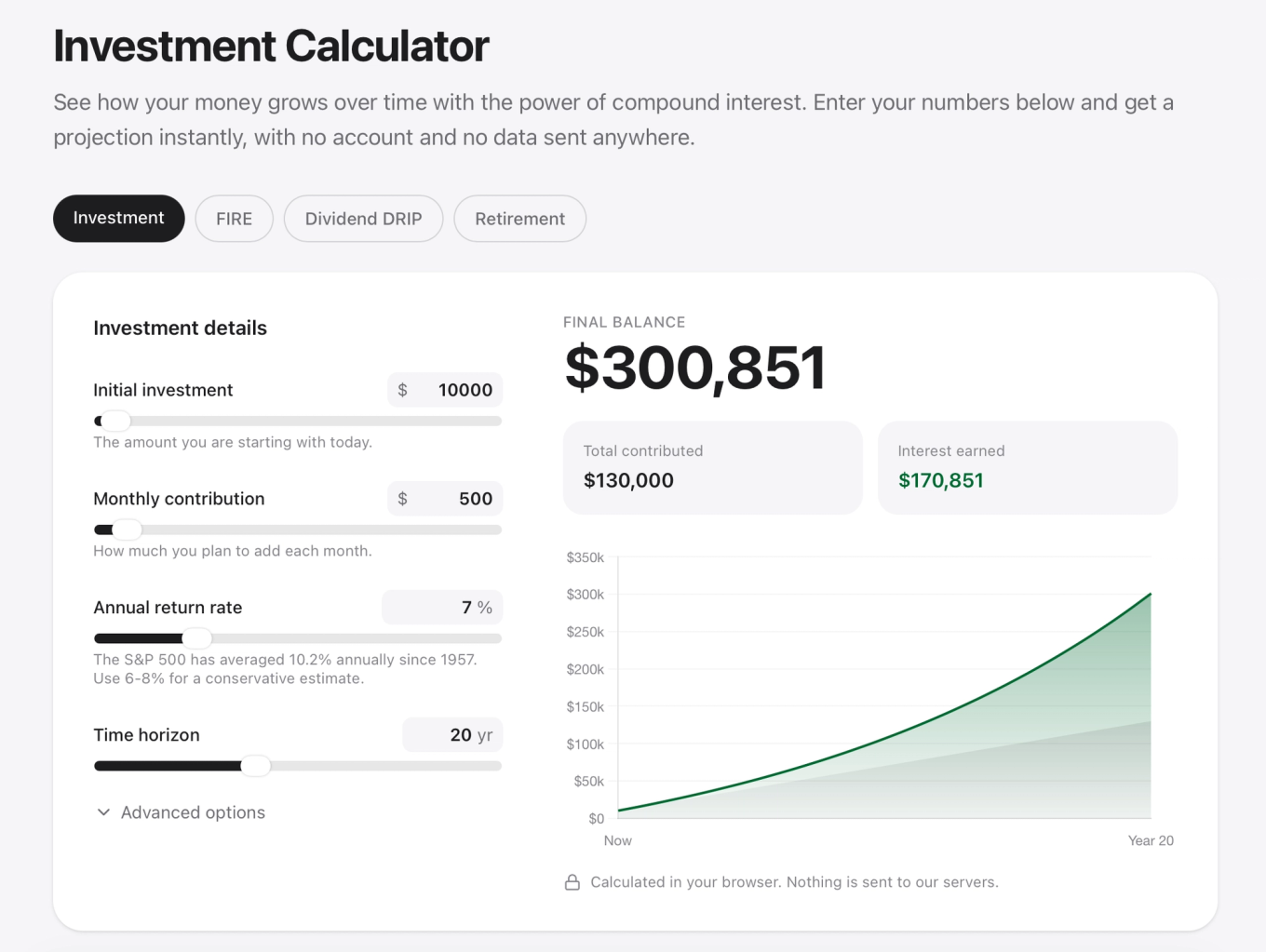

Try the DecentWealth Investment Calculator to model your own scenario. Plug in your starting balance, your monthly contribution, and your expected return rate. It runs in your browser, nothing is stored, nothing is sent anywhere. Just math and your numbers.

Frequently Asked Questions

How much will $500 a month be worth in 20 years?

Is 7% a realistic return rate for long-term investing?

Why does compound interest seem slow at first?

How do I track compound growth in my actual portfolio?

What if I can only invest $100 or $200 a month?

Track your portfolio privately

Stocks, crypto, real estate, and more. No account required.