4 Free Investment Calculators That Don't Ask for Your Email

Key Takeaway

DecentWealth offers four free financial calculators: an Investment Calculator for compound growth projections, a FIRE Calculator to find your financial independence number, a Dividend DRIP Calculator to model reinvestment compounding, and a Retirement Calculator that shows both the accumulation and drawdown phases. All four run in your browser with zero data collection. No account, no email, no server calls. Your numbers never leave your device.

You know the drill. You search "investment calculator," click the first result, and before you can type a single number, there's a popup asking for your email. Then a cookie banner. Then a "create a free account to save your results" wall. By the time you get to the actual calculator, you've already handed over more personal data than a TSA checkpoint.

We built four financial calculators at DecentWealth that skip all of that. They run entirely in your browser. No backend, no server calls, no accounts, no data collection. You move a slider, you get a number. That's it. That's the product.

Here's what each one does and when to use it.

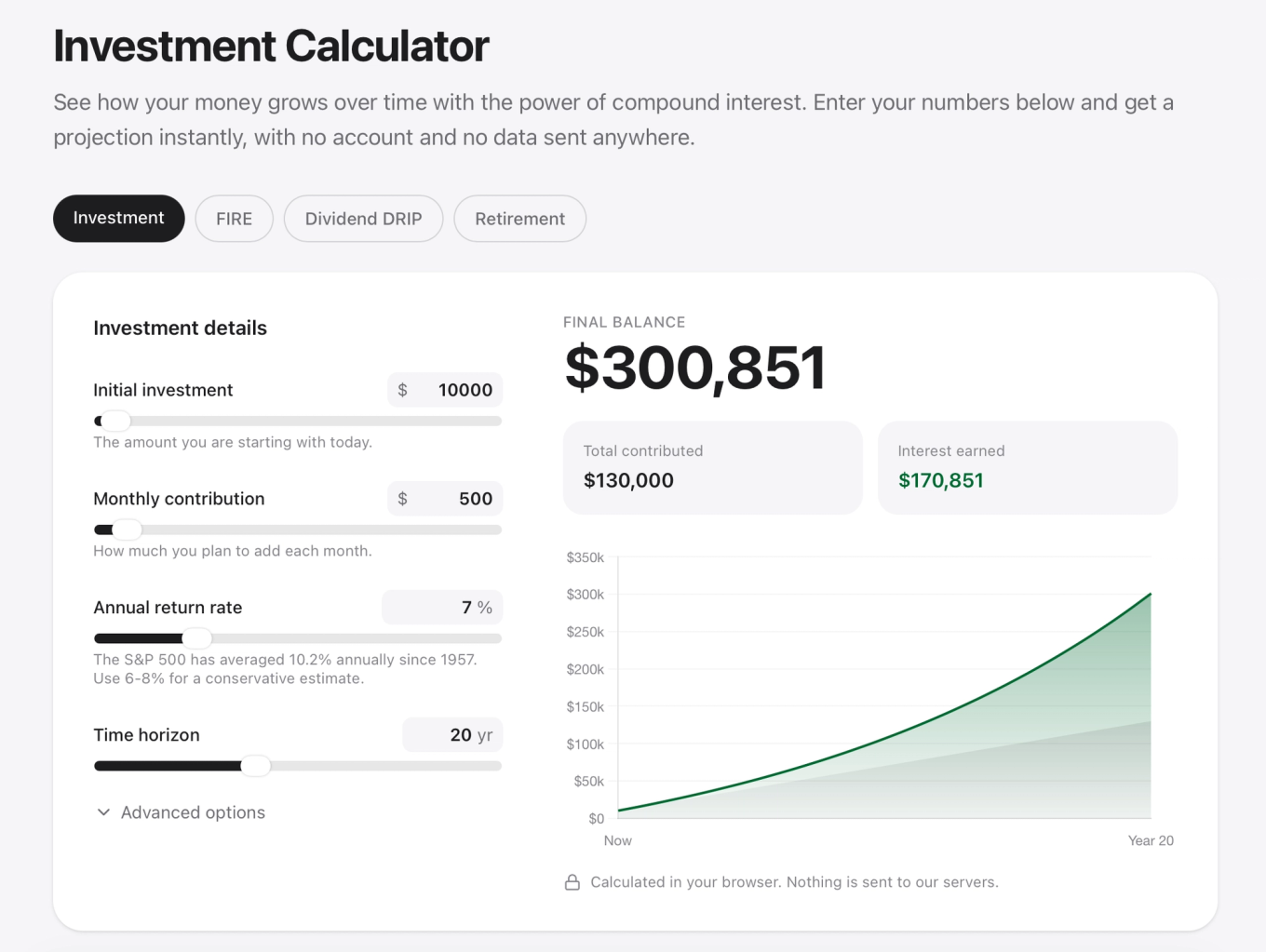

Investment Calculator: How Much Will My Money Actually Grow?

This is the one you want when you're staring at your brokerage account wondering what happens if you just keep doing what you're doing for the next 20 years.

Enter your starting balance, monthly contribution, expected return rate, and time horizon. The calculator splits the result into what you contributed versus what compound interest added on top. That split is the whole point. It's one thing to know your projected balance. It's another to see that your money literally made more money than you did.

Quick example: $500 a month at 7% annual return, starting from zero. In 30 years, you'll have contributed $180,000 of your own cash. Your projected balance? Roughly $567,000. The market did more heavy lifting than you did. That's compounding in one screenshot.

You can also toggle between monthly, daily, and annual compounding in the advanced settings, though for most stock and ETF investors, monthly is the realistic assumption.

Best for: Anyone wondering "is my savings rate enough?" or "what if I started five years earlier?" (Spoiler: the answer to that second one is always painful.)

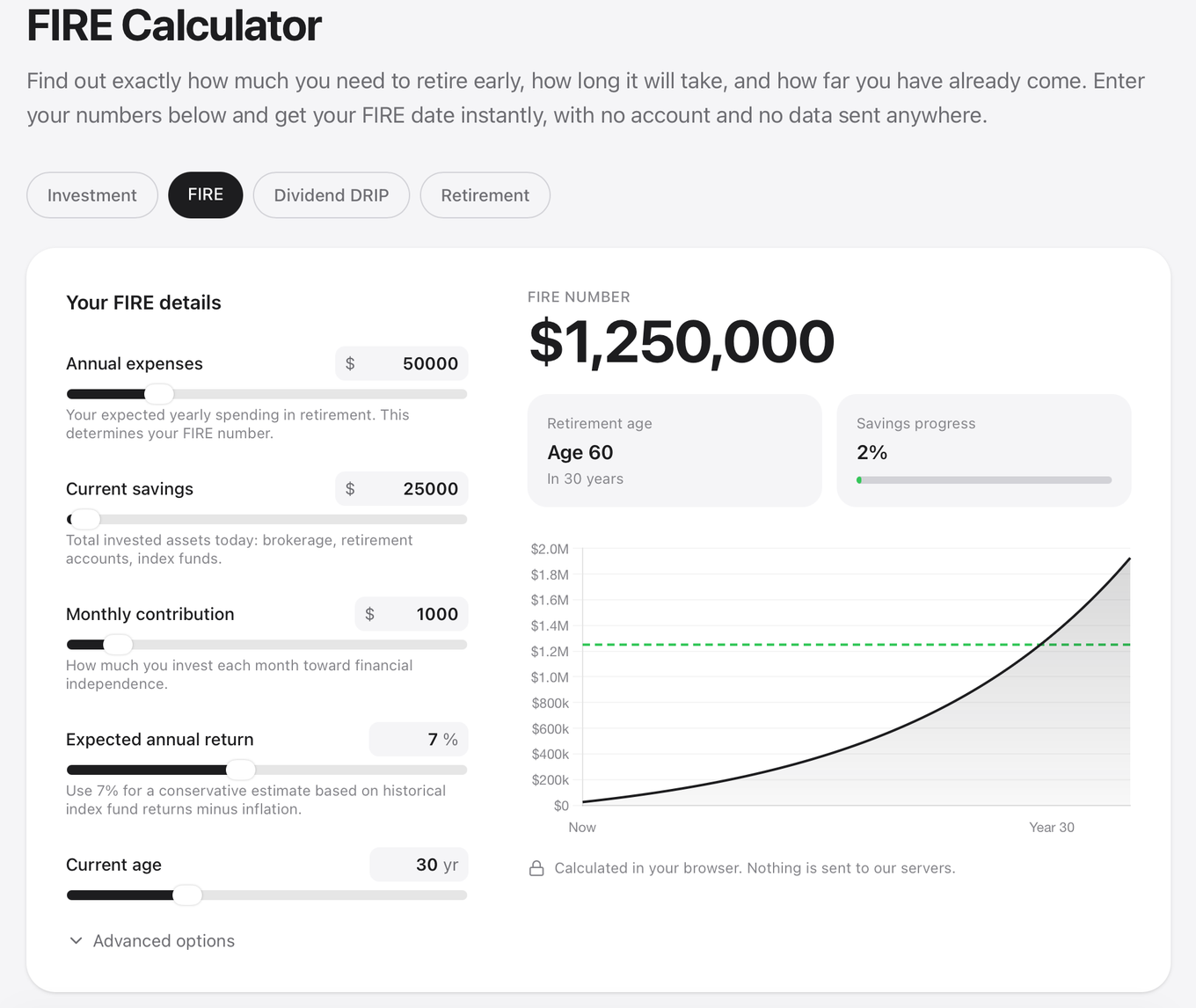

FIRE Calculator: When Can You Actually Stop Working?

FIRE stands for Financial Independence, Retire Early. The concept is simple: save and invest aggressively until your portfolio is large enough to cover your expenses forever.

The math behind it is even simpler. Your FIRE number equals your annual expenses divided by your safe withdrawal rate. At the standard 4% rate (based on the 1994 Trinity Study), that's your annual spending multiplied by 25.

Spend $50,000 a year? Your target is $1,250,000. Spend $80,000? You're looking at $2,000,000. The fastest way to lower the target isn't earning more. It's spending less. A $10,000 reduction in annual expenses drops your FIRE number by $250,000.

The DecentWealth FIRE Calculator takes your current savings, monthly contributions, expected returns, and age, then tells you exactly when you'll cross the finish line. It also shows your progress as a percentage, which is either motivating or humbling depending on where you stand.

If you're planning a retirement longer than 30 years (which most early retirees are), drop the withdrawal rate to 3% or 3.5% in the advanced options. The 4% rule was designed for traditional 30-year retirements, not for people trying to retire at 38.

Best for: Anyone who has ever Googled "can I retire early" at 2 AM. Also useful for the Lean FIRE crowd ($40K/year lifestyle) and the Fat FIRE crowd ($100K+ lifestyle). Just change the expenses input and see how the timeline shifts.

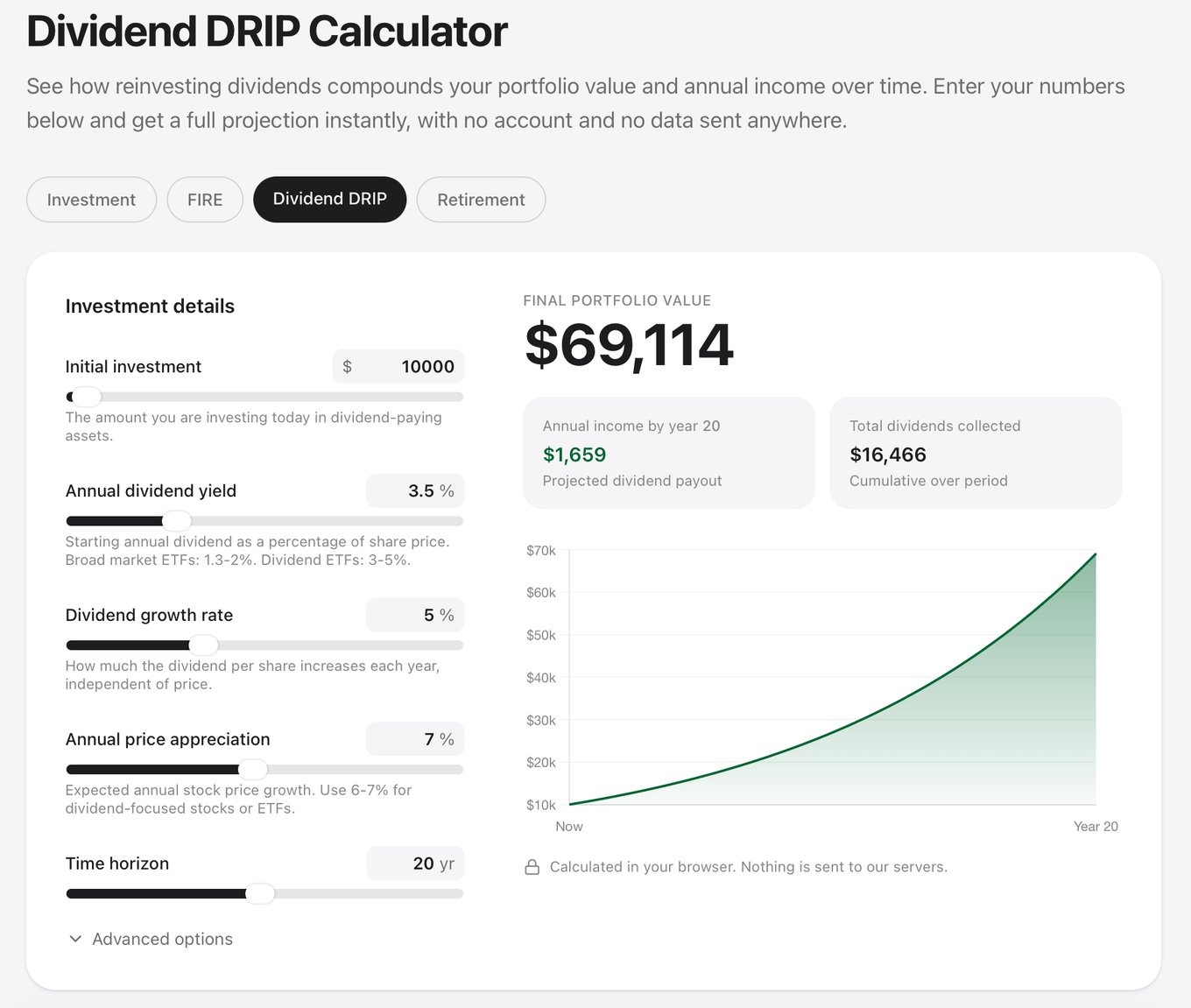

Dividend DRIP Calculator: Your Shares Making Shares

DRIP stands for Dividend Reinvestment Plan. Instead of taking your dividends as cash, you use them to buy more shares. Those new shares pay their own dividends. Those dividends buy more shares. Repeat for 20 years and you've got a snowball that rolled itself downhill while you were busy living your life.

This calculator models the full DRIP effect over time. You enter your initial investment, starting dividend yield, dividend growth rate, stock price appreciation, and time horizon. It shows you the final portfolio value, your projected annual dividend income, and the total dividends collected over the entire period.

Here's where it gets interesting. A $10,000 investment with a 3.5% yield and 7% annual price growth turns into roughly $56,000 over 20 years with DRIP enabled. Without reinvestment, price appreciation alone gets you to about $38,700. The gap comes entirely from reinvested dividends buying shares that then pay their own dividends.

The advanced options let you add a monthly contribution and apply a dividend tax rate. Set the tax rate to 0% if you're modeling a Roth IRA or 401(k) where dividends compound tax-free. Use 15% to 20% for a taxable brokerage account.

One thing to pay attention to: dividend yield vs. dividend growth rate. They're different inputs and they matter in different ways. A stock with a modest 2% yield but 8% annual dividend growth will pay you more per share within a decade than one starting at 5% yield with only 2% growth. Over the long run, growth beats starting yield nearly every time.

Best for: Dividend investors who want to see the actual compounding effect of reinvestment, not just "trust me, DRIP works." Also great for comparing high-yield vs. high-growth dividend strategies side by side.

Try the Dividend DRIP Calculator

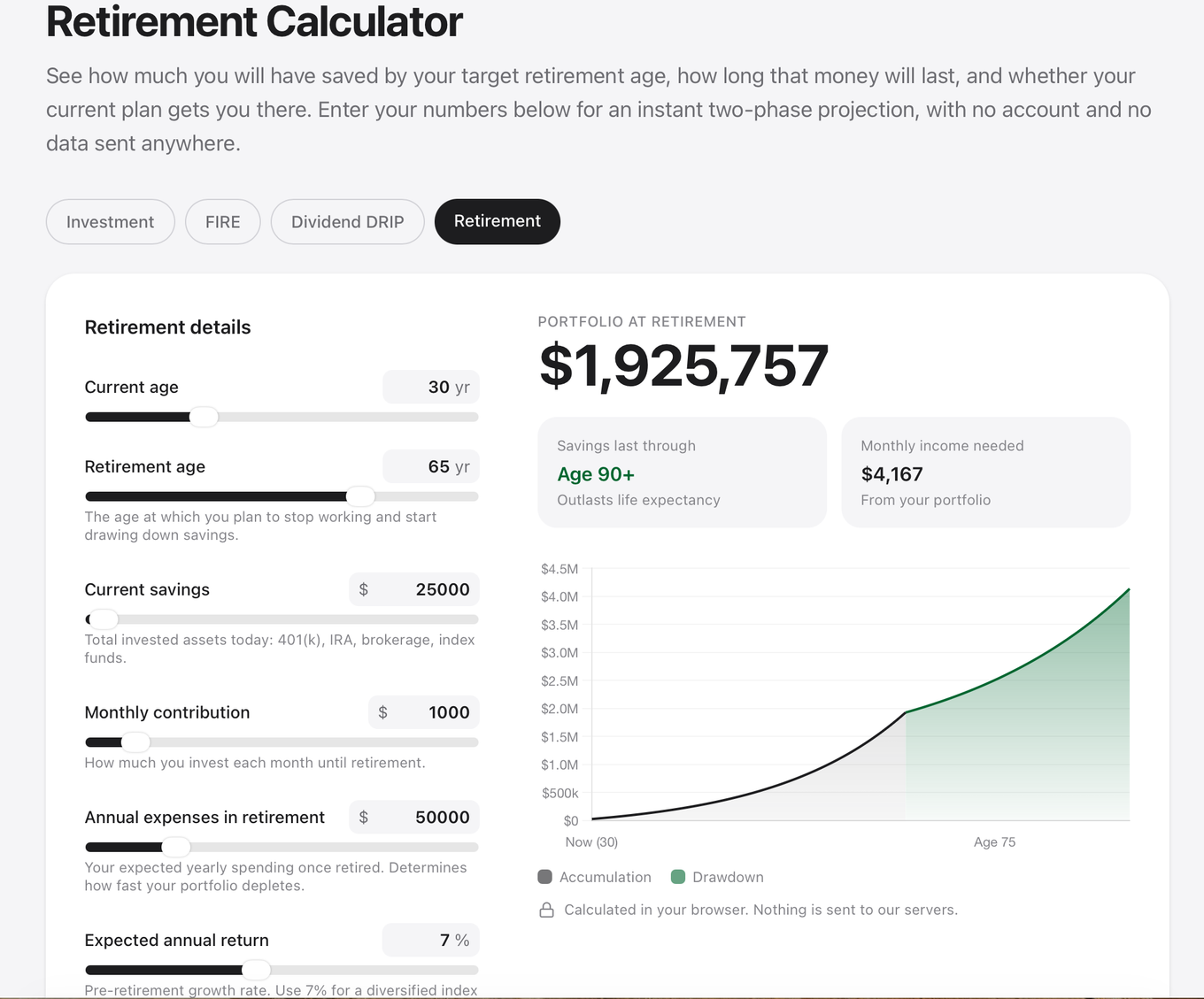

Retirement Calculator: Will Your Money Outlive You?

This one models both sides of the equation. Phase one: accumulation (your working years, where you're saving and investing). Phase two: drawdown (retirement, where you're spending down the portfolio). Most calculators only show you phase one. This one shows you the moment where the line peaks and starts heading back down.

Enter your current age, retirement age, savings, monthly contribution, expected expenses in retirement, and your pre-retirement return rate.

The calculator projects your portfolio at retirement and then models how long that money lasts based on your withdrawal rate and a separate post-retirement return assumption (which is typically lower, since retirees usually shift to more conservative allocations).

The two-phase chart is the most useful part. The dark section is accumulation. The green section is drawdown. If the green line hits zero before your life expectancy, you have a problem. If it stays positive through age 90+, you're in good shape.

A practical tip: The post-retirement return slider is the one most people ignore and the one that matters most for longevity. Bumping it from 4% to 6% can add a decade to how long your savings last. That's not a recommendation to take on more risk in retirement. It's a reason to think carefully about your asset allocation strategy after you stop working.

Best for: Anyone with a specific retirement age in mind who wants to answer "will I actually be okay?" rather than just "how big will my portfolio be?" If your main question is "when can I retire?" use the FIRE Calculator instead. If your question is "will I run out of money?" this is the one.

Why We Built These (and Why They're Private)

Most financial calculator sites are lead generation tools wearing a math costume. The calculator is the bait. Your email is the catch. Your inbox full of "financial advisor" cold emails is the consequence.

We built these because we think financial tools should just work. No signup, no email capture, no "create an account to unlock your results." Every calculation runs in your browser using standard financial formulas. Your inputs never leave your device. You can literally disconnect from the internet, and every calculator will keep working.

This is the same philosophy behind the DecentWealth app itself: a private net worth dashboard and portfolio overview for iPhone and iPad that stores everything on your device. No accounts, no servers storing your holdings, no analytics tracking your behavior.

Run your calculations without running your data through someone else's servers. A decent amount of privacy for people with a decent portfolio.

Which Calculator Should You Use?

It depends on the question you're trying to answer:

"How much will my investments be worth in X years?" Use the Investment Calculator. Straightforward compound growth projection with a clear breakdown of your contributions vs. market returns.

"When can I stop working?" Use the FIRE Calculator. It calculates your Financial Independence number and shows exactly how many years of saving and investing stand between you and freedom.

"How much passive income will my dividends generate?" Use the Dividend DRIP Calculator. It models the snowball effect of reinvesting dividends over time, showing both portfolio growth and income growth.

"Will my savings last through retirement?" Use the Retirement Calculator. It models both the saving phase and the spending phase, so you can see whether your plan actually works all the way through.

All four are free. All four are private. All four work right now, no signup required.

Ready to Track the Real Thing?

Calculators are great for planning. But at some point, you stop projecting and start investing. When you do, DecentWealth tracks your actual portfolio across stocks, ETFs, digital assets, retirement accounts, and more. Everything stays on your iPhone. No account, no cloud storage, no data collection.

__________________________________________________________________________________

This article is general information, not personalized investment advice. Gold prices move, tax rules vary by country, and we're a portfolio tracker, not your financial advisor. Do your own homework, and talk to a professional before making decisions about your money.

Frequently Asked Questions

Are these financial calculators really free?

Do I need to create an account to use the calculators?

Is my financial data private when I use these calculators?

What's the difference between the Investment Calculator and the Retirement Calculator?

What's the difference between the FIRE Calculator and the Retirement Calculator?

What is a FIRE number?

What is DRIP and why does it matter?

Can I use these calculators on my phone?

Track your portfolio privately

Stocks, crypto, real estate, and more. No account required.