Escape the 9-to-5: The 2026 Guide to the FIRE Movement

Key Takeaway

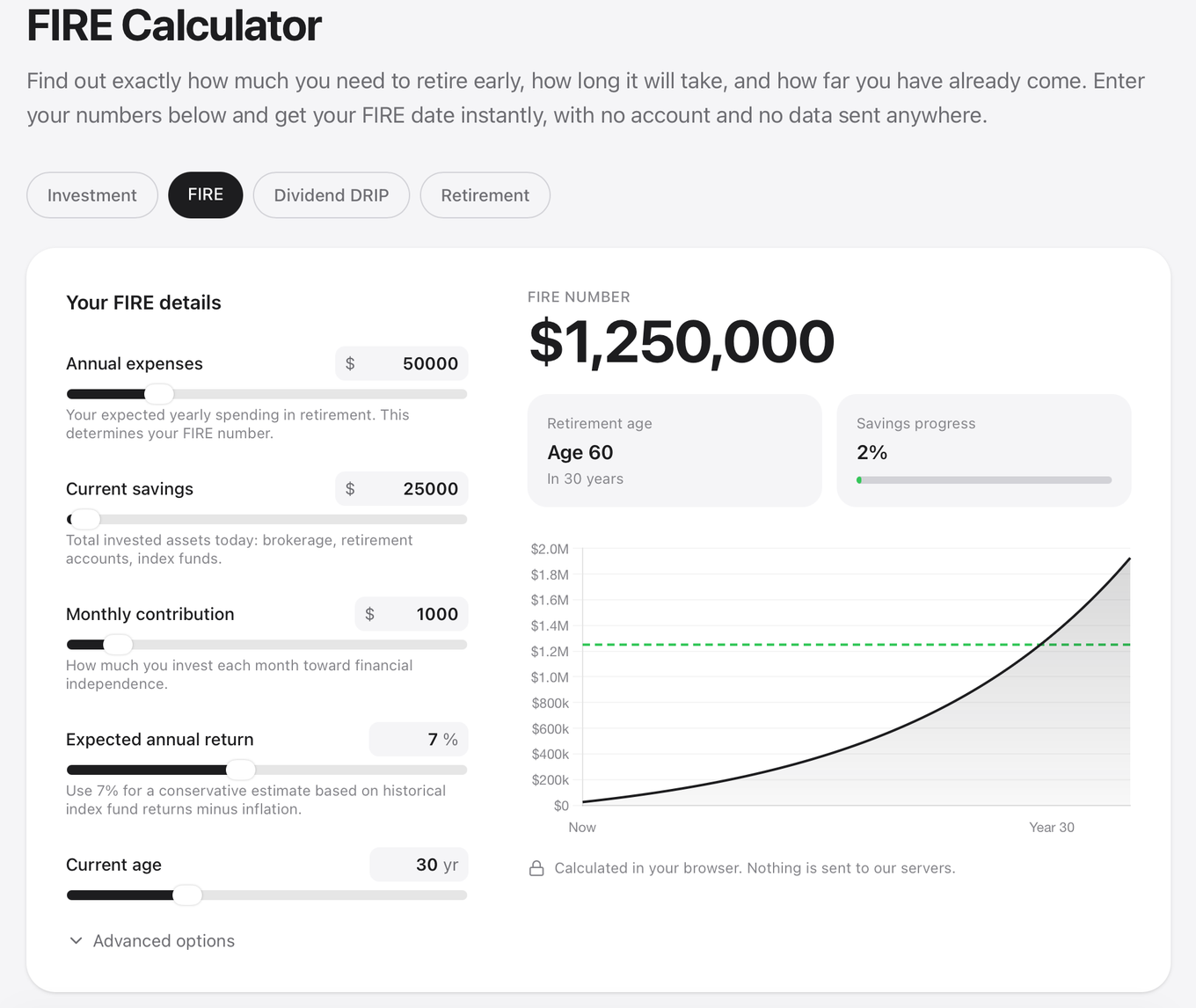

FIRE (Financial Independence, Retire Early) is built on one formula: save 25 times your annual expenses, invest it, and withdraw 4% per year. Spend $50K a year? Your target is $1.25 million. The real lever isn't income, it's savings rate. At 50%, you're looking at roughly 15 years to independence. The movement has four main paths: Lean FIRE (minimalist, under $40K/year), Fat FIRE (comfortable, $100K+), Barista FIRE (part-time work fills the gap), and Coast FIRE (stop saving once compound growth handles the rest). The catch? Healthcare before 65 is expensive, the 4% rule wasn't built for 50-year retirements, and early market crashes can wreck the math. If you're planning your number, the DecentWealth FIRE Calculator runs entirely in your browser with no account and no data collection. When you're ready to track the real portfolio, DecentWealth keeps everything on your device.

The FIRE Movement in 2026: A Practical Guide for People Who'd Rather Not Work Until They Die

The traditional retirement plan goes something like this: work for 40 years, save a little along the way, retire at 67, and hope the math works out. For a lot of people under 40, that plan sounds less like a goal and more like a life sentence.

The FIRE movement (Financial Independence, Retire Early) offers a different proposition. Save aggressively, invest consistently, and build a portfolio large enough to cover your expenses without a paycheck. Not at 67. At 45. Or 40. Or whenever the math says you're done.

This isn't a get-rich-quick scheme. It's a get-rich-slowly-on-purpose scheme. And in 2026, it's gone from Reddit niche to something a quarter of young professionals are actively thinking about.

A Goldman Sachs survey found that 25% of Gen Z respondents plan to retire before 55. Whether they'll pull it off is another conversation. But the intent is real, and the math is surprisingly simple.

What FIRE Actually Means (And What It Doesn't)

FIRE is not about quitting work and staring at a wall. Most people who reach financial independence keep doing something. They freelance, build projects, volunteer, travel, or just work on their own terms. The point isn't to stop being productive. The point is to make work optional.

Three terms you'll see everywhere in FIRE conversations:

FIRE Number. The total portfolio size you need to never work for money again. Calculated as your annual expenses divided by your safe withdrawal rate. At a 4% withdrawal rate, that's your annual spending multiplied by 25.

The 4% Rule. A guideline from financial planner William Bengen's 1994 research, later supported by the Trinity Study. The idea: withdraw 4% of your portfolio in year one, adjust for inflation each year after, and your money should last at least 30 years. It's not a guarantee. It's a planning framework that survived every historical 30-year market period in the U.S.

Savings Rate. The percentage of your take-home pay that goes into investments. The average American saves somewhere around 5% to 8%. FIRE practitioners typically target 50% to 75%. That gap is the entire game.

The Math of "I'm Out"

The core formula is almost offensively simple:

FIRE Number = Annual Expenses x 25

If you spend $50,000 a year, you need $1,250,000. If you spend $80,000 a year, you need $2,000,000. If you spend $40,000 a year, you need $1,000,000.

Notice something? Your income doesn't appear in the formula. Your expenses do. That's the counterintuitive truth of FIRE: the fastest way to financial independence isn't earning more. It's needing less. Every $10,000 you cut from your annual spending drops your target by $250,000.

Once you hit your number, you withdraw 4% per year. On a $1,250,000 portfolio, that's $50,000 annually. Your remaining investments keep growing, and in most historical scenarios, your portfolio actually gets larger over time despite the withdrawals.

If you're planning a retirement longer than 30 years (which you probably are, if you're reading this at 30), consider using a 3% to 3.5% withdrawal rate for extra margin. That means multiplying your expenses by 28 to 33 instead of 25. More conservative? Yes. More likely to let you sleep at night for the next 50 years? Also yes.

Want to run your own numbers? The DecentWealth FIRE Calculator shows your FIRE number, your projected retirement age, and your current progress. No account, no email, no data sent anywhere.

Four Flavors of FIRE

Not everyone pursuing financial independence is trying to live off beans and library books. The movement has branched into distinct approaches, each with its own trade-offs.

Lean FIRE

The minimalist path. You keep annual expenses under $40,000 (sometimes well under) and retire as fast as possible. The portfolio target is smaller, the timeline is shorter, and the lifestyle is deliberately simple.

This works well for people who genuinely enjoy living lean. It works less well for people who are just white-knuckling it through the savings phase and plan to "reward themselves later." If your post-retirement budget makes you miserable, you haven't retired. You've just become an unemployed person who hates their life.

Fat FIRE

The comfortable path. Annual expenses of $100,000 or more, which means a target portfolio of $2.5 million and up. The tradeoff is obvious: you need to earn significantly more, save longer, or both. But the retirement lifestyle looks a lot like your current one (or better). Fat FIRE is essentially traditional wealth-building with a deadline attached.

Barista FIRE

The hybrid path. You've saved enough to cover most of your expenses through investment returns, but you work a part-time job to fill the gap or keep health insurance. The name comes from the idea of pulling espresso shots at a coffee shop, though in practice it could be any low-stress, part-time gig. Healthcare is a real consideration here.

According to the Kaiser Family Foundation, a 62-year-old purchasing ACA coverage paid an average of $1,116 per month for a silver-tier plan in 2025. A part-time job that includes health benefits can save you over $13,000 a year in premiums alone.

Coast FIRE

The most psychologically freeing variant. You invest aggressively early in your career, and at some point your portfolio is large enough that compound growth alone will carry it to a full retirement number by age 65, with zero additional contributions. You still work to cover current expenses, but you stop saving. No more aggressive savings rate. No more optimizing every line item in your budget. You just coast.

Coast FIRE is less about retiring early and more about removing the financial pressure from the middle of your career. You can take a lower-paying job you actually enjoy, go part-time, or switch fields without worrying about the retirement math.

Why Savings Rate Matters More Than Income

There's a reason FIRE communities are obsessed with savings rate and relatively quiet about salary. Your savings rate determines two things at once: how much you invest each year and how much you need to live on (and therefore how big your target needs to be).

A high earner who spends everything has a massive FIRE number and nothing saved toward it. A moderate earner with a 50% savings rate has a modest FIRE number and is putting half their income toward it every month.

Here's the rough math, assuming a 5% real (inflation-adjusted) return:

At a 50% savings rate, you can reach financial independence in roughly 15 to 17 years. At 70%, that drops to around 8 to 10 years. At 25% (still well above average), you're looking at 30+ years.

The point isn't to make you feel bad about your current savings rate. It's to show you which lever actually moves the timeline. Getting a 10% raise feels great, but if your expenses rise to match, your FIRE date doesn't budge. Cutting your expenses by 10% while keeping your income the same moves the date forward twice: once because you're saving more, and once because your target got smaller.

The Stuff Nobody Talks About (But Should)

Healthcare Is Expensive When You're Not Employed

This is the single biggest non-investment challenge for early retirees in the U.S. If you retire at 40, you have 25 years before Medicare kicks in at 65. That's a long time to pay full price for health insurance. ACA marketplace plans exist, but they're not cheap, and subsidies depend on your income (which in FIRE terms means your withdrawal amount, not your portfolio size).

Many FIRE planners build healthcare costs directly into their annual expense estimate. If you don't, your FIRE number is wrong.

The 4% Rule Wasn't Designed for 50-Year Retirements

Bengen's original research and the Trinity Study analyzed 30-year retirement periods. If you're retiring at 35 and planning to live to 90, that's 55 years. A 4% withdrawal rate gets less reliable over longer horizons. This is why many early retirees use 3% to 3.5%, which requires a larger portfolio but dramatically reduces the risk of running out.

Sequence of Returns Risk Is Real

The biggest threat to a FIRE plan isn't a bad year in the market. It's a bad few years at the start of retirement. If your portfolio drops 30% in your first two years of withdrawals, you're pulling money from a shrunken base, and the math gets ugly fast. A cash buffer covering 2 to 3 years of expenses can protect against this. So can flexibility: being willing to cut spending temporarily or pick up some income during a downturn.

You Might Get Bored

This one catches people off guard. After years of optimizing every dollar and counting down to the finish line, some people hit their number and realize they don't know what to do with themselves. Financial independence is a math problem. A meaningful life is not. Worth thinking about before you get there, not after.

How to Actually Track Your Progress

The spreadsheet phase is fine for a while. But once you're tracking a real portfolio across multiple accounts, brokerages, and asset types, you need something better.

This is what DecentWealth was built for. It's a portfolio tracker for iPhone and iPad that lets you see your entire financial picture in one place: stocks, ETFs, crypto across 18 blockchains, real estate, retirement accounts, cash, and debt. Your net worth, your allocation, your dividend income, your performance. All of it.

And here's the part that matters for the privacy-conscious FIRE crowd: DecentWealth doesn't have accounts. There's no signup, no email, no server storing your data. Everything lives on your device, protected by Face ID. No company sees your portfolio. No analytics track your behavior.

If you're still in the planning phase, start with the FIRE Calculator to find your number and your timeline. Use the Investment Calculator to model different savings scenarios. And when you're ready to track the real thing, download DecentWealth and keep your financial life where it belongs: on your phone, behind your face.

We provide a decent amount of privacy for people with a decent portfolio.

Frequently Asked Questions

Is the FIRE movement still realistic with 2026 inflation rates?

What do FIRE followers do about health insurance?

Do I have to stop working entirely?

Is it too late to start if I am in my 40s?

Track your portfolio privately

Stocks, crypto, real estate, and more. No account required.